The quick accounting method Gst/HST was introduced by Canada Revenue Agency (CRA) to help small businesses calculate their net tax for GST/HST purposes in a simplified manner.

When you use the GST/HST quick method for your business, you still charge the applicable GST and HST on your supplies of taxable goods and services. However, to calculate the amount of GST/HST payable, multiply the revenue from your supplies (including the GST/HST) for the reporting period by the quick method remittance rate, or rates, that apply to your situation.

The remittance rates of the quick method are less than the applicable rates of GST/HST that you charge. This means that you remit only a part of the tax that you collect, or that is collectible. As a result, in many cases, this can result in significant savings every year.

How will The Quick Method Benefit You?

- Calculating GST/HST remittances and filing GST/HST returns becomes much easier because it eliminates the need to record and report the actual GST/HST paid or payable on most purchases.

- the quick method allows small businesses to calculate tax payable by simply multiplying revenue with the quick method remittance rates applicable. Therefore, instead of paying all GST/HST collected on sales, small business can apply the reduced remittance rate under GST/HST quick method. This benefits many small businesses to save money on tax remittance.

- By using the the quick method, your business is also entitled to a 1% credit on the first $30,000 of revenue (including GST/HST) you earned each fiscal year.

- Generally speaking, most goods and service based small businesses are eligible to use the quick method and found the quick method is quicker and easier to use than the general method under most circumstances.

- This method also eases the pain of a GST/HST Audit because of its simplicity. You should still keep all your receipts!

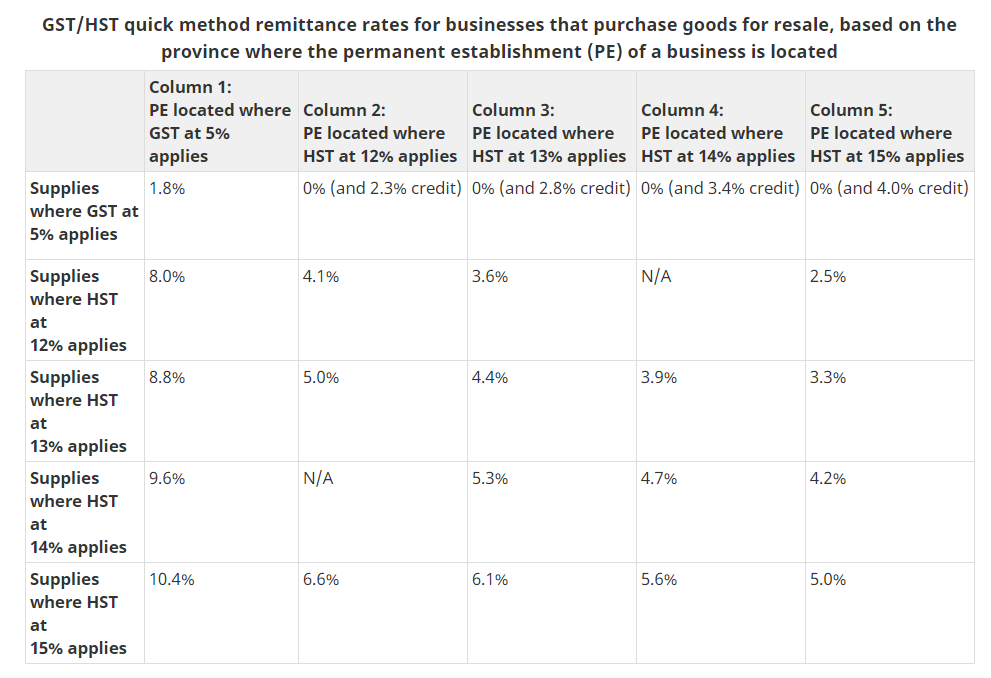

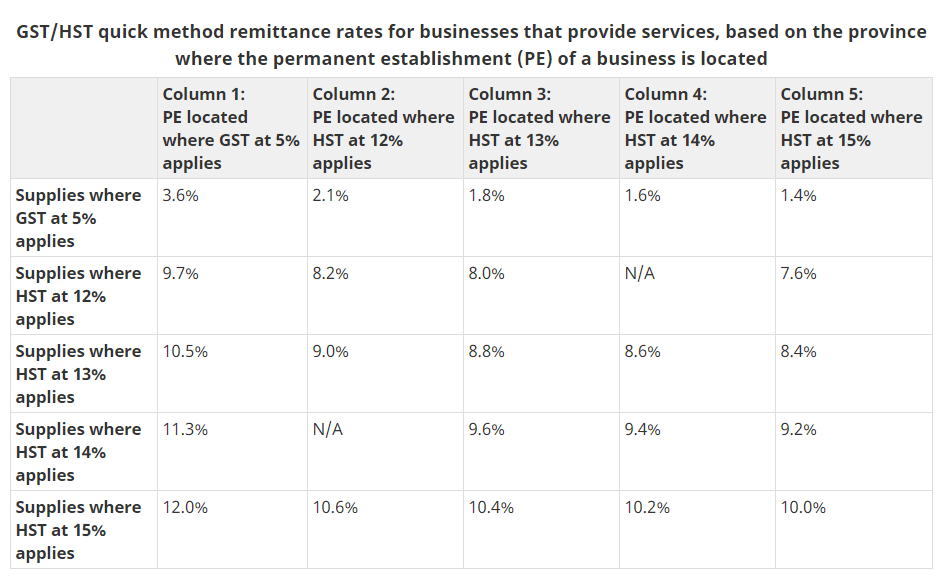

What Are The Quick Method Remittance Rates?

The following tables represents the applicable remittance rates for small businesses located in difference provinces of Canada. For example, for business in Ontario, the quick method remittance rate is 8.8% for a service-based business and 4.4% for a goods-resale business.

Quick Method Eligibility Criteria

Below is a checklist to see if the GST/HST quick method applies to your business, you can use the quick method if you meet all of the following conditions:

- You have been in business continuously throughout the 365-day period ending immediately before your current reporting period.

- You did not revoke an election of the quick method or the simplified method for claiming ITCs during that 365-day period.

- Your annual revenues (including the GST/HST) from worldwide taxable supplies (including zero-rated supplies), and those of your associates, are not more than $400,000

Business types that cannot use the quick method:

- persons that provide bookkeeping, financial consulting, tax consulting or tax return preparation services in the course of the person’s commercial activity

- persons that provide legal, accounting or actuarial services in the course of their professional practice

- listed financial institutions

- charities

- public institutions

- non–profit organization with at least 40% government funding in the year (qualifying non–profit organizations)

- municipalities or local authorities designated as a municipality

- public colleges, school authorities, or universities, that are established and operated other than for profit

- hospital authorities, facility operators, or external suppliers

GST/HST Quick Method Election

The quick method election can be made online on CRA via the My Business Account or by Represent A Client.

Annual GST/HST filers have to make the election by the first day of the second fiscal quarter for the business. Monthly or Quarterly GST/HST filers have to make the election by the due date of the return for the reporting period in which you begin using the quick method.

The election stays in place until you meet the criteria above, or your voluntarily revoke the election, which can also be done via CRA online.

ITCs That You Can Claim Under Quick Method

- purchases of real property and improvements to real property

- purchases of capital property (other than real property), such as computers and vehicles, and improvements to capital proper

- purchases of eligible capital property and improvements to eligible capital property (before January 1, 201

- purchases on which GST/HST became payable before your quick method election took effect, if the time limit to claim the amounts has not expired

- goods sold by an auctioneer or an agent on your behalf where the auctioneer or agent has to account for the tax

- goods you are considered to have bought to use only in your commercial activities if:

- a non-resident, who is not registered for the GST/HST, transferred them to you, after paying tax on them

- you provided a commercial service on the goods and then sold them, acting as an agent for the non-resident and collecting the GST/HST

Contact Abdullah CPA for further guidance.